WHY COMPETITIVE ADVANTAGES ARE TYPICALLY TEMPORARY?

- To survive and thrive an organization must create a competitive advantages.

A product or service that an organization's customers place a greater value on than similar offerings from a competitor.

First-mover advantage

Occurs when an organization can significantly impact its market share by being first to market with a competitive advantage.

- Organizations watch their competition through environmental scanning

The acquisition and analysis of events and trends in the environment external to an organization

- Three common tools used in industry to analyse and develop competitive advantages include :

-Porter's three generic strategies

-Value chains

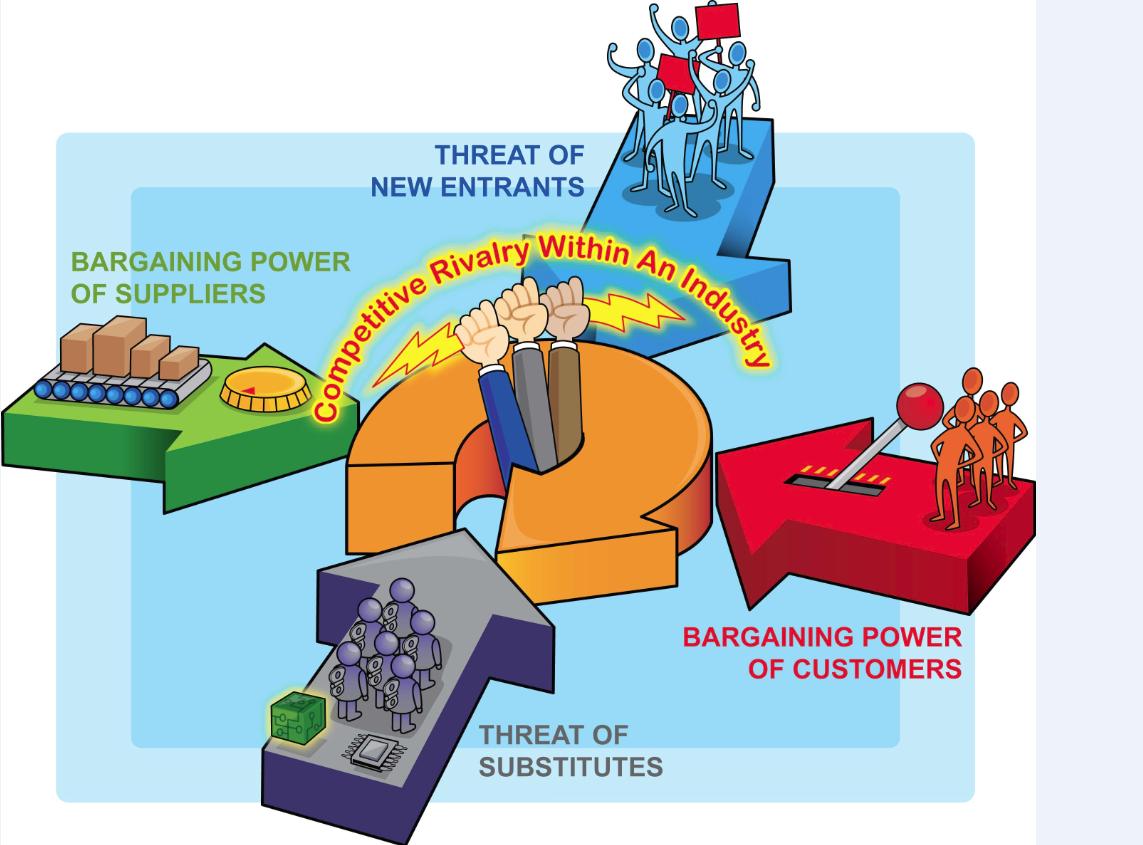

The Five Forces Model Evaluating Business Segments

- Portal's Five Forces Model determines the relative attractiveness of an industry

Buyer Power

- High when buyers have many choices of whom to buy from and low when their choices are few.

- Way to reduce buyer power is through loyalty programs

2) Switching costs - costs that can make customers reluctant to switch to another product or service.

Supplier Power

- High when buyers have few choices of whom to buy from and low when their choices are many.

- Organizations that are buying goods and services in the supply chain can create a competitive advantages by locating alternative supply sources (decreasing supplier power) through B2B marketplaces

- Two types of business to business (B2B) marketplaces

2) Reverse auction - an auction format in which increasingly lower bids are solicited from organizations willing to supply the desired product or service at an increasingly lower price.

Threat of Substitute Products or Services

- Threat of Substitute Products or Services - high when there are many alternatives to a product or service and low when there are few alternatives from which to choose

Switching costs - costs that can make customers reluctant to switch to another product or service.

Threat of new entrants

- Threat of new entrants - high when it is easy for new competitors to enter a market and low when there are significant entry barriers to entering a market

Rivalry among Existing Competitors

- Rivalry among Existing Competitors - high when competition is fierce in a market and low when competition is more complacent.

- Although competition is always more intense in some industries than in others, the overall trend is toward increased competition in just about every industry.

- Organizations typically follow one of Porter's three generic strategies when entering a new market.

Value Creation

- Once an organization chooses its strategy, it can use tools such as the value chain to determine the success or failure of its chosen strategy

Value chain - views an organization as a series of processes, each of which adds value to the product or service for each customers.

- Customers determine the extent to which each activity adds value to the product or service

- The competitive advantage is to :

- Target low value-adding activities to increase their value

- Target low value-adding activities to increase their value- Perform some combination of the two

No comments:

Post a Comment